The majority of us will spend many years developing our wealth; however, very few of us consider what we would do should we become unable to manage that wealth ourselves due to illness, an accident, or a condition associated with aging. The lack of planning for this situation can lead to significant issues for family members, such as delay, additional expense, and/or confusion surrounding who will have the power to act on your behalf.

Therefore, incapacity planning becomes essential. Incapacity planning allows you to put the proper legal tools into place ahead of time (i.e., powers of attorney and/or health care directives) so that the persons you trust to make decisions for you will be able to do so when your circumstances change.

In addition to having international assets or complicated financial arrangements, one may need to create structures such as offshore trusts. If used properly, these types of structures allow for the continued management of your assets without requiring your direct oversight.

Key Takeaways

- Planning for incapacity includes preparing the legal and financial structures that will be needed if you become disabled or mentally incapacitated.

- The core legal structures for planning ahead for disability include powers of attorney, advance health care directives, guardianship plans, and trust agreements.

- The use of offshore trusts is another tool to provide an added level of protection and continuity for your global wealth structure.

- Combining all these legal structures helps prevent the courts from intervening in your long-term financial plan.

- Offshore asset protection trusts are commonly used by individuals with international assets they want to protect from creditor claims, while still being able to obtain qualified professional help on an ongoing basis.

What Is Incapacity Planning?

Planning for incapacity means taking legal and financial steps to allow someone else to act for you when you are unable to take care of yourself due to serious illness, injury, accident, age-related cognitive decline, or temporary medical issues.

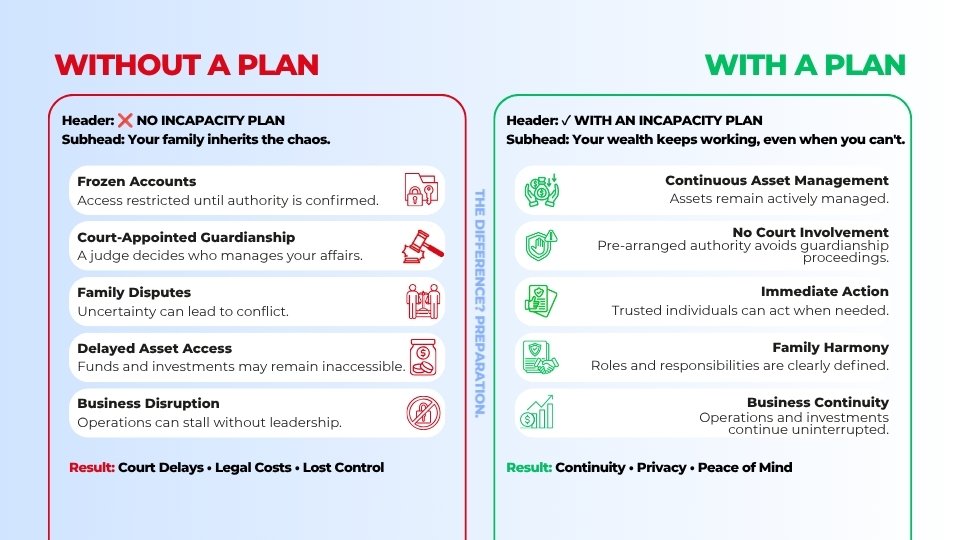

If there is no plan, banks and other financial institutions, along with most government departments, will require a court order before permitting another person to act as your agent regarding your assets and/or make decisions for you.

The resulting delays and potential disputes among relatives make it even more complicated for wealthy people worldwide who hold assets in multiple countries. Since each country has its own laws governing trust/asset protection, many multinational families include an offshore trust as part of their overall incapacity strategy. For instance, in the UK, this is typically handled through the Court of Protection system under the Mental Capacity Act 2005 framework.

Why Incapacity Planning Matters for International Wealth and Offshore Trust Structures

Planning for disability will be particularly significant where an individual’s overseas investments are located. Many countries have unique rules governing how business or other matters are conducted; if the person managing those overseas assets suffers a sudden loss of capacity, it could quickly become complicated.

Examples include:

- Overseas portfolios of stocks, bonds, commodities etc.

- Overseas real estate holdings

- Private companies or family businesses (with operations outside the settlor’s home jurisdiction)

- Bank accounts located outside their home jurisdiction

- Intellectual property holdings (e.g., patents, trademarks etc.)

If all of these assets were managed by that person (in their personal capacity), there would likely be considerable logistical difficulties immediately upon their becoming disabled. In particular, banks and financial service providers may delay giving access to funds on accounts until they obtain proper legal documentation confirming which parties have authority over the account(s).

However, with regard to offshore trusts, the situation is somewhat different. Trust law principles and legal frameworks, such as the OECD, are widely used in common-law jurisdictions and several offshore financial centers. As the trustee was appointed pursuant to a previously agreed-upon set of terms to administer the trust, he/she/it can continue to manage the assets under the same terms regardless of whether the settlor becomes incapable of managing his/her affairs.

Core Legal Tools for Effective Incapacity Planning

Legal tools that support effective disability planning include several types of legal arrangements that, when used together, form a complete disability plan. The legal tools address various aspects of decision-making and asset management.

Durable Power of Attorney

Using a durable power of attorney (POA) allows one to designate another individual they trust to make financial or legal decisions on their behalf. In the UK, for example, the equivalent of a durable power of attorney is a Lasting Power of Attorney (LPA), which is officially governed by the UK government and registered with the Office of the Public Guardian.

An individual designated as an agent or attorney-in-fact may be granted the authority to:

- Manage bank accounts

- Pay bills and other obligations

- Oversee investment portfolios

- Sign contracts or agreements

- Interact with banking and/or financial institutions

The term “durable” means that the authority granted will continue to exist regardless of whether the individual has become disabled.

For individuals who hold property through offshore trusts or international banking relationships, having a POA may enable the representative to interact with the trustee(s) of such a trust or relationship when necessary.

Healthcare Directives and Living Wills

Health care directives deal exclusively with health-related issues; they do not address health care-related issues relative to your personal finances or assets. Commonly covered within a health care directive are:

- Your preference regarding how you wish to receive medical treatment

- Deciding whether to permit life-sustaining treatments or critical care

- Instructions for how you would prefer to die at the end of your life

- Appointing an individual whom you trust to make decisions concerning your health care on your behalf.

Multiple instruments exist globally, including in the United States, where advance directives are legally recognized across all states.

Clear, current health care directives can relieve the burden upon your loved ones and ensure that your wishes regarding your health care are respected – even if you cannot express those wishes personally.

Guardianship and Conservatorship Planning

When an individual is incapacitated but lacks sufficient documentation of their disability, courts may appoint a guardian or conservator. Guardianship/conservatorship proceedings typically include:

- Court hearings

- Medical evaluations

- Ongoing monitoring by court officials

- Periodic reporting requirements

Although guardianship/conservatorship can offer some degree of protection for an incapacitated individual, this option is very expensive and time-consuming. If an individual properly plans ahead — perhaps using offshore trust structures — the need for judicial intervention can be greatly diminished.

The Role of Offshore Trusts in Incapacity Planning

A trust is a legal structure in which assets are transferred to a trustee who manages them for the benefit of designated beneficiaries.

When assets are placed into offshore trusts, they are administered according to the terms of the trust deed and the laws of the chosen jurisdiction.

This structure provides several advantages in incapacity planning:

- Trustees continue managing the assets regardless of the settlor’s personal situation

- Investment decisions remain consistent with the trust’s objectives

- Beneficiaries can still receive distributions according to the trust terms

- Asset protection measures remain in place

Because trustees have legal control over the trust assets, the structure continues functioning even if the settlor is temporarily or permanently unable to manage personal affairs.

For this reason, offshore trust structures are often used in international estate planning and cross-border wealth management.

FREE CONSULTATION

on offshore structures and jurisdictions

that would best meet your

asset protection goals.

on offshore structures and jurisdictions that would best meet your asset protection goals.

Why Trustees Can Continue Acting After Incapacity

There are numerous benefits to using trust-based planning, but one of the most significant is separating legal ownership from beneficial ownership (who actually owns the assets). Once you place your assets into a properly established trust, then the assets will be titled in the name of the trustee, while formerly they were titled in the name of the settlor. If the settlor is unable to conduct their own business dealings or sign documents on their own behalf due to disability or incapacity, the trustee may continue to act as if the settlor had performed these actions. By doing so, many of the problems and disruptions created when an individual owns their assets personally will be eliminated. Many of the problems created by the need for a bank or other financial institution to require authorization before taking any action regarding an individual’s account will also be eliminated.

Benefits of Using Offshore Asset Protection Trusts

The primary advantage of an offshore asset protection trust is that it allows you to protect your wealth by providing a means for a third party (the trustee) to manage your assets on your behalf.

As such, offshore asset protection trusts provide you with several important advantages, including:

- Wealth management continuity

- Protection from certain legal claims

- Privacy and confidentiality

A professional trustee will be appointed to oversee the trust. This provides assurance regarding how your assets will be managed across borders.

Additionally, because the Trustee is required to administer your assets under the terms of the trust agreement, if you become incapacitated, an offshore asset protection trust will continue to operate. Therefore, they can be a valuable resource for high-net-worth individuals, entrepreneurs, investors, and families who have complex international wealth holdings.

Comparison of Incapacity Planning Tools

The following table outlines some of the methods available under law to assist individuals with the planning process for managing incapacitation.

| Tool | Purpose | Key Benefit |

| Power of Attorney | Authorizes someone to manage financial affairs | Immediate decision-making authority |

| Healthcare Directive | Guides medical decisions | Ensures treatment preferences are respected |

| Guardianship Planning | Court-appointed oversight if no documents exist | Legal protection but involves court process |

| Offshore Trusts | Professional asset management structure | Continuity of wealth management |

| Offshore Asset Protection Trusts | Protect and manage international assets | Long-term asset protection |

It should be noted that combining two or more of these methods can provide greater protection than using a single method.

Offshore Trust Jurisdictions and Incapacity Planning

As a result of the development of laws and regulations in various countries that support offshore trust administration and international asset protection planning, there are now many countries where such planning can occur. Some common countries providing this type of planning include:

| Jurisdiction | Notable Features |

| Nevis | Strong asset protection legislation |

| Cayman Islands | Well-established international trust law |

| British Virgin Islands | Popular for international wealth structures |

| Bermuda | Long tradition of trust administration |

These jurisdictions often provide modern legal frameworks that allow trustees to manage assets efficiently while maintaining privacy and compliance.

Example Scenario: Incapacity Planning with Offshore Trusts

Let us suppose that a businessman had made investments across several countries. To better enable him to manage his assets, protect them, and ensure their administration was carried out as per his wishes after his death, the majority of his global portfolio (all of his international real property interests and all of his foreign investment accounts) was held in a single offshore trust.

Before creating this offshore trust strategy, the businessman created additional documentation for the benefit of himself and other members of his family:

- A durable power of attorney

- Advance healthcare directives

- Family governance documents

Over time, the businessman experiences a serious medical condition and becomes temporarily incapacitated by reason of sickness or injury, and thus cannot act independently. As he has transferred the majority of his assets into an offshore trust (thereby subjecting himself to the terms of the trust), the trustee will have the authority to exercise discretion and take such action as is permitted under the trust to continue administering and distributing those assets. The family may therefore continue to administer the businessman’s financial affairs without incurring any further costs, rather than incurring high court costs to obtain permission to continue acting on the businessman’s behalf.

Risks of Not Having an Incapacity Plan

Not preparing for your own incapacitation could result in significant problems.

Some of the most common problems include:

- Your bank account(s) are being frozen

- Being appointed a court guardian

- Family members fighting over what to do with you/your affairs

- Significant delays in accessing your money/assets/businesses, etc.

- Businesses/investments are becoming disrupted

If you have international wealth, these issues could be compounded because of jurisdictional differences. Offshore trusts and other types of international asset protection structures can be useful in reducing many of these risks by helping ensure continued management of your assets.

Best Practices for Effective Incapacity Planning

Most incapacity plans consist of more than just one document. Creating a comprehensive plan requires taking a larger view. This should allow those who need to make your financial and personal decisions in the event of an unanticipated circumstance to do so as quickly and easily as possible.

The following are some practical ways to make this process easier:

- Create durable powers of attorney (DPAs) which provide authorization for trusted persons to act on your behalf when making any necessary financial or legal decisions.

- Create healthcare directives/living wills that clearly outline your wishes regarding medical treatment in the future.

- Examine how all of your large assets are owned and/or structured, particularly when they are held across multiple jurisdictions.

- Individuals with international wealth may also want to consider utilizing offshore trusts as part of their overall asset management strategy.

- Check your legal documents periodically to ensure they are consistent with your current status.

These tools, working together, create a more stable environment for protecting your assets and facilitating smooth decision-making in the event that your circumstances change.

When Offshore Trusts Are Most Useful

Although everyone can benefit from incapacity planning, there are specific times and situations when offshore trust structures will be most useful for you.

Some of those examples include:

- International entrepreneur

- Global investors

- Multi-generation family wealth managers

- Individuals owning assets in multiple countries

- Owner(s) of a privately held company with international operations

At this point, offshore trusts may be used to maintain stability and consistency during difficult times by providing a mechanism to protect and manage assets on behalf of the owner.

Summary

Good incapacity planning will ensure that all necessary financial and personal decisions are made to assist an individual who has lost the ability to make them. There are many legal mechanisms available to support effective incapacity planning, including, but not limited to, powers of attorney, healthcare directives, and trusts.

For individuals with significant wealth or who hold assets across multiple countries, using offshore trusts can provide an additional layer of protection and stability. As long as the trustee follows the trust’s terms, the offshore trust will operate independently of the settlor’s capacity or lack thereof.

Using an offshore trust as one component of a larger legal strategy will help protect an individual’s overall wealth while also helping them achieve their long-term financial objectives.

FAQ

What is incapacity planning?

Incapacity planning involves developing both financial and legal strategies (such as establishing powers of attorney, health care directives, and various types of trusts) that enable others to act on your behalf to handle your daily living needs if you become incapacitated.

How do offshore trusts help with incapacity planning?

Offshore trusts support incapacity planning by allowing the trustee(s) to manage the trust assets in accordance with the predetermined terms of the trust. As such, the wealth structure established through an offshore trust continues to function regardless of whether the settlor has become incapacitated.

Do offshore asset protection trusts replace powers of attorney?

Offshore asset protection trusts are intended to be used as one component of an overall incapacity plan, along with other tools such as powers of attorney and health care directives.

Who should consider incapacity planning?

Any person who possesses significant assets, business interests, or international wealth structures may need to establish an incapacity plan in order to ensure the continued protection of their financial and personal interests.